The municipal bond market, traditionally a bastion of stability and tax-advantaged fixed-income investing, is showing signs of strain that many investors seem unwilling to fully acknowledge. As we move deeper into 2025, the sheer volume of new municipal debt issuance is reaching unprecedented levels. With an expected $50 billion in supply just for June and overall forecasts nudging past $580 billion for the year, the pressure on valuations and yields is palpable. This is not a simple story of healthy growth or investor appetite; it’s an uncomfortable reality where supply is aggressively pushing yields higher and suppressing tax-exempt returns.

The fundamental issue here is the record supply. It’s a classic case of too much product flooding a finite market. The Barclays strategists’ observation that tax-exempt municipal bonds have “underperformed” against U.S. Treasuries due to the heavy issuance is a tacit admission that the market mechanics are tilted unfavorably. Even though the Treasury market has weakened somewhat with yields climbing, munis have failed to keep pace, igniting valuations and prompting some volatility. This dynamic suggests a risk that tax-exempt bonds might not be the safe haven many investors assume.

Disturbing Yield Dynamics Amidst Heavy Issuance

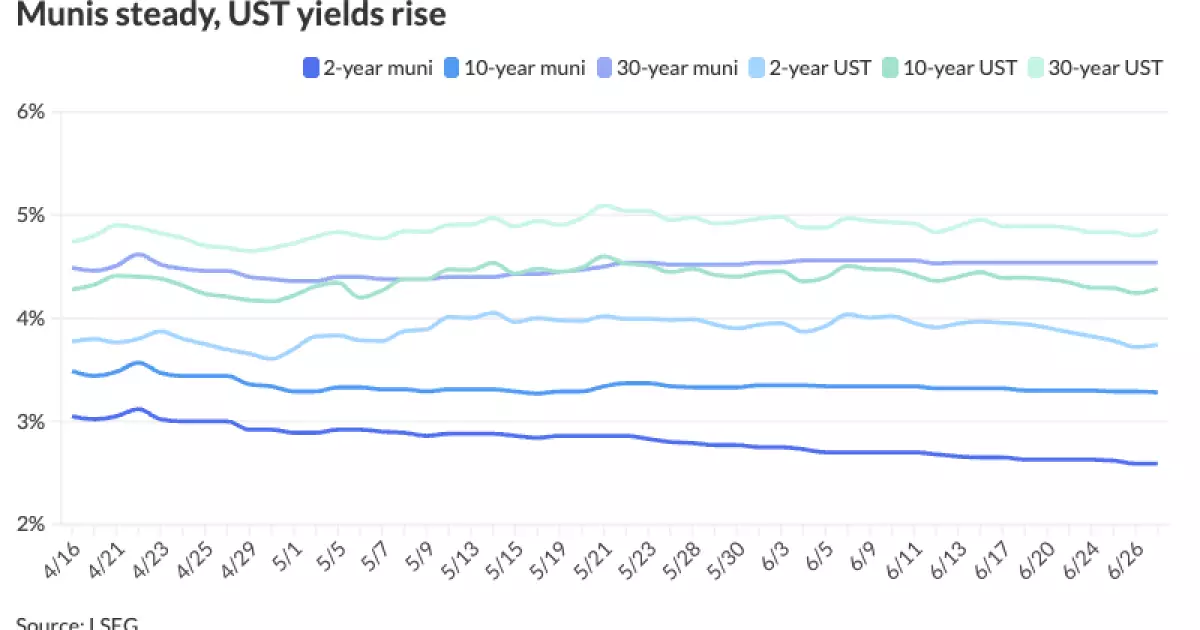

The yield ratios between municipals and Treasuries are especially revealing. Traditional wisdom dictates that municipals should offer relatively better value due to their tax advantages, yet the data shows troubling trends: the 10-year muni-to-UST ratio has climbed close to 77%, with the 30-year nearing 94%. This means municipals are yielding almost as much as Treasuries—a sign of undervaluation or elevated risk in the muni market—or both. What’s particularly troublesome is that this ratio has widened alongside increased issuance, indicating an effective imbalance where buyers struggle to absorb the avalanche of new bonds without demanding significantly more yield.

For cautious investors inclined toward muni bonds for their perceived safety and tax efficiency, these ratios raise a red flag. Are municipals truly undervalued bargains, or are the risks—stemming from borrower quality, liquidity, and economic headwinds—being underpriced? My suspicion leans toward the latter. The heavy issuance is not taking place in a vacuum; it reflects growing fiscal pressures on local governments, and a burgeoning risk of credit deterioration that few seem keen to price adequately.

The Illusion of Seasonal Strength: Why July and August May Not Be What They Seem

Historically, midsummer has been a relatively favorable period for municipals, with supply-demand dynamics supportive of prices. Yet, the current outlook casts doubt on whether this seasonal pattern will hold in 2025. While analysts predict that July and August might see technicals strengthen courtesy of redemptions and coupon payments counterbalancing issuance, this equilibrium looks fragile.

The key risk is complacency. Investors might mistakenly rely on past seasonality, expecting municipal bonds to rebound or at least stabilize. But given the volume of fresh supply and the ongoing fiscal challenges faced by many municipalities—from pension liabilities to infrastructure backlogs—this optimism could prove misplaced. If high issuance continues unabated or if credit concerns gain traction, the typical summer “breather” may evaporate, exposing investors to sharp pricing corrections just as they try to lean into the market.

Valuations and Risks: The False Comfort of “Good Value”

Statements from strategists that municipals “remain the only fixed income asset class with negative total returns year-to-date” and yet “offer good value at current valuations” warrant skepticism. It may be tempting for some investors, especially those influenced by conservative biases, to see deep discounts as an opportunity to accumulate, but ‘value’ cannot be divorced from context.

This is not a market where cheap means safe—it often means fear and uncertainty are building beneath the surface. The resurgence of issuance is driven by increased borrowing needs from strained municipal budgets rather than vibrant economic growth or expansionary fiscal policies. Furthermore, the proposition that “rates aren’t a concern and investors should get longer” could backfire if interest rates continue to climb or if inflationary pressures persist. The underperformance so far this year is a warning signal, not a mere blip.

We are in a period where complacency could be costly unless investors are willing to constantly reevaluate credit fundamentals and the macroeconomic environment. The municipal market’s apparent discount hides a complex interplay of fiscal stress, high issuance, and shifting yield expectations that demand a more vigilant approach.

Primary Market Frenzy and Impending Risks

Finally, looking at the upcoming calendar, notable issuers like the Massachusetts Bay Transportation Authority and the Los Angeles Unified School District are preparing to tap the markets with large bond sales. Such high-profile offerings are illustrative of trends in public sector finance: major metropolitan entities are taking advantage of investor demand to refinance or raise new capital, possibly to patch budget deficits or fund long-delayed projects.

While these deals attract attention and liquidity, they also concentrate risk. When municipal entities depend heavily on debt markets to maintain operations, they become more vulnerable to shocks like rising interest rates or downturns in tax revenue. The reality is that this binge of issuance risks exacerbating imbalance and could amplify vulnerability within the muni bond space—especially if underlying economic conditions sputter.

Investors stepping into this environment must recognize that the municipal bond market in 2025 is far from placid. The convergence of massive issuance, rising yields, questionable credit quality, and strategic mispricing points toward a need for disciplined selectivity and a skeptical eye. It’s no longer enough to lean on historical norms or tax benefits. The stakes have risen, and only the prudent will navigate this complex landscape unscathed.