Recently, the municipal bond market has displayed a surprising resilience amidst the shifting tides of the U.S. economy. On a recent Monday, municipal bond yields remained relatively stable, even as U.S. Treasuries experienced slight declines. This juxtaposition raises a critical question of how national monetary policy, specifically the Federal Reserve’s ongoing adjustments, impacts municipal bonds. Municipal bonds hold a distinctive position as they typically carry certain tax advantages, which further complicates the dynamics when Treasury yields fluctuate.

Notably, the ratios between munis and Treasuries indicate varying levels of demand across different maturities. The two-year municipal-to-Treasury ratio was recorded at 62%, demonstrating a cautious market outlook. Such ratios can serve as a bellwether for investor sentiment, reflecting broader macroeconomic trends and fiscal health. In general, a higher ratio signifies a demand for safety and security, often at the expense of yield; investors may prefer tax-exempt securities when they believe that market conditions may deteriorate.

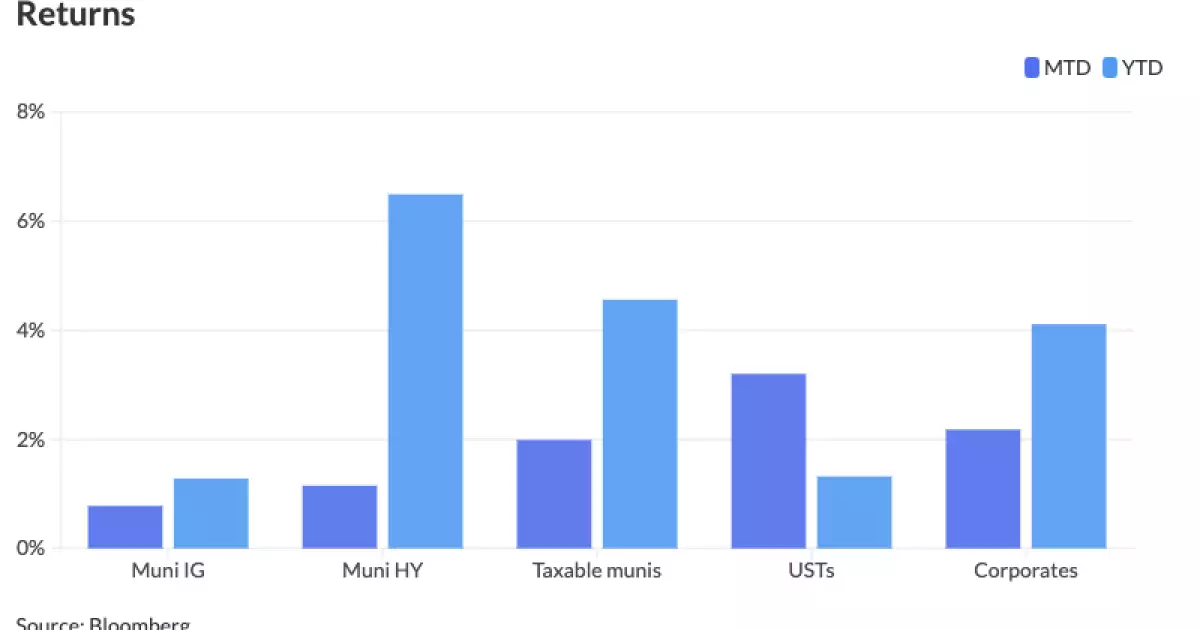

As we approach the end of August, the municipal market has gained 0.78% this month, bringing year-to-date returns to an even 1.28%. This represents a significant turnaround from the same period last year when municipalities witnessed a distressing loss of 1.79%. Investors are likely weighing this year’s performance against last year’s struggles as they reassess their portfolio strategies. Jason Wong, a vice president at AmeriVet Securities, noted the dramatic shift in market dynamics resulting from the Federal Reserve’s previous rate hike strategy aimed at curbing inflation. These past actions set a backdrop for the current market shift, as investors now anticipate a dovish pivot in interest rates.

Furthermore, the ongoing rise in municipal yields—averaging an increase of 26 basis points across the curve—indicates a volatile environment. Particularly, 10-year municipal notes reflect more considerable movements, highlighting the sensitivity of long-dated securities to both changes in economic forecasts and Federal Reserve policy adjustments.

The market’s recent behavior closely follows Fed Chair Jerome Powell’s recent statements suggesting it may be time to cut interest rates. This anticipation has triggered a downward shift in both Treasury yields and investor interest in munis, as they adjust their expectations regarding future rate changes. Historically, such signals from the Federal Reserve can lead to increased bond activity as investors seek to capitalize on potential price appreciation before rate cuts.

Despite the sluggish summer session, characterized by lower trading volumes, the municipal market has shown signs of renewed vigor. Chris Brigati, senior vice president at SWBC, pointed out that the previous week underwhelmed in terms of activity partly due to summer holidays. Still, the anticipated speeches from Powell seem to have injected some interest into the market, helping municipals catch up to UST price fluctuations.

Looking ahead, the primary market indicates a steady flow of new issuances, which will continue to be critical for market liquidity. The upcoming weeks promise a variety of significant offerings, including various general obligation bonds from states like California and infrastructures like the North Texas Tollway Authority. These offerings can serve as a barometer for market health and investor risk appetite.

Interestingly, the upcoming issuance includes refunding bonds, a tactic municipalities employ to take advantage of lower interest rates and reduce borrowing costs. This strategic maneuver aims to provide fiscal relief to local governments, further solidifying the importance of municipals in maintaining public infrastructure and services.

The municipal yield curve remains an essential tool in understanding market conditions. Refinitiv MMD data indicates a stable outlook for shorter maturities while noting some fluctuations among longer durations, which may reflect investor concerns about future economic growth and inflation. The yield compression at the shorter end signifies that buyers are willing to accept lower yields in exchange for the security that municipals traditionally offer.

As we draw closer to the Labor Day holiday and the seasonal transition that follows, careful observation of market movements and investor behaviors in response to Fed policies will be crucial for understanding the broader implications for municipals. For investors, this evolving landscape invites strategic positioning that aligns with both short-term gains and long-term fiscal prudence.

While municipal bonds might seem stable against the backdrop of fluctuating Treasuries, the subtle shifts prompted by Federal policy and investor sentiment highlight the complexities that govern this segment of the market. As the end of summer approaches, the interplay of supply and demand, alongside fiscal strategies, warrants continued scrutiny for those who seek to navigate the intricate world of municipal finance.