Despite the nostalgia surrounding municipal bonds as a safe haven for conservative investors, the current market environment reveals troubling ambivalence rather than robust vitality. Municipal debt showed only faint signs of improvement at the start of the week, with yields creeping up marginally while U.S. Treasuries gained ground and equities rose. However, this modest uptick belies an overarching theme of lethargy and uncertainty. The dynamics of muni versus Treasury yields reveal ratios that hint at underlying undervaluation, yet the catalyst to convert that value into meaningful performance is conspicuously absent.

Most market observers, like Birch Creek strategists, describe the muni space as stuck in a cycle of “limited volatility and price movements.” This stagnation is neither typical for a sector that usually thrives on well-timed newsflows or changing fiscal environments nor favorable for investors seeking opportunities. The lack of clear drivers for muni outperformance underscores a key dilemma: investors recognize the cheap valuations but remain cautious about acting decisively without a reliable market impetus.

The Illusion of Outperformance Fueled by Technical Support

Monthly data reveals that muni mutual funds have seen nine consecutive weeks of inflows, yet the totals are modest, barely scratching the surface needed for a true rally. The recent $76.9 million inflow pales beside broader capital markets’ scale and does little to spark meaningful spreads compression or yield tightening. What’s more, the year-to-date performance remains below zero, eroding confidence that the muni sector has fully recovered from spring’s sharp dislocations.

The flow of principal and interest payments maturing in July offers the most promising technical support. With a massive $40 billion in principal and $14 billion in interest expected, the reinvestment cash presents some relief for the market. This strong supply of liquidity, particularly concentrated in states like California, New York, and Florida, should theoretically underpin demand and improve conditions. Yet despite these substantial cash flows, the primary market’s tepid issuance levels—especially around the July 4th holiday—limit the ability of the market to absorb new supply effectively.

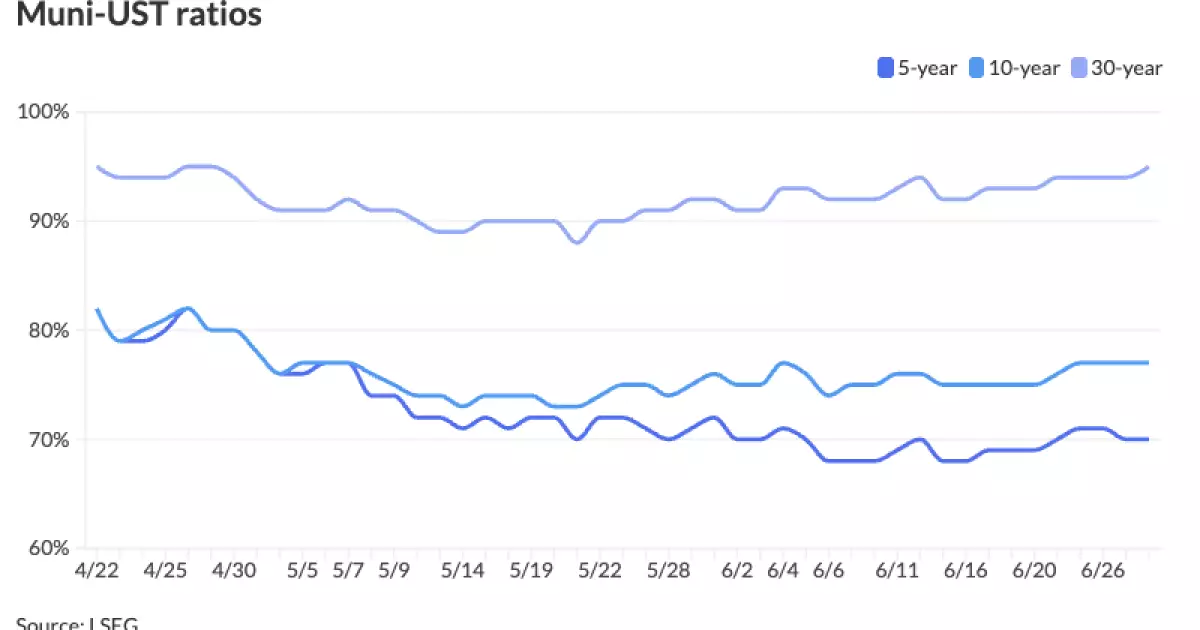

The “Cheap But Stuck” Paradox

Perhaps the most vexing aspect of the muni market is this paradox of attractiveness versus inertia. Ratios of muni to Treasury yields are at multi-year lows, with long-term munis offering after-tax yields exceeding 8% on some high-grade deals. Such yields should be a siren call to yield-hungry investors seeking tax-advantaged income, especially against a backdrop of historically high inflation and volatile equity markets.

Instead, market participants remain on the sidelines, constrained by a lack of conviction in macroeconomic direction and political risk. There is a palpable absence of a definitive catalyst—whether fiscal, regulatory, or monetary—that could ignite a surge in demand. Without that ignition, the muni market’s “cheapness” is little more than a static data point, insufficient to inspire robust buying.

This hesitancy reflects a broader hesitance in center-right liberal circles wary of unchecked municipal debt expansion amid uneven fiscal discipline in various states. There’s a growing unease that some issuers are leveraging low rates to mask unsustainable spending, which could backfire, especially if economic growth falters.

Primary Market: Quiet Before the Storm?

Though the primary market volumes are currently low, signs point to potentially significant upcoming activity. Deals from major issuers such as the California Community Choice Financing Authority and the Washington Metropolitan Area Transit Authority signal that significant capital projects are still pressing ahead. Additionally, later July includes substantial offerings from New York State and the New York City Transitional Finance Authority, potentially shifting supply dynamics dramatically.

These large issuances could either exacerbate bondholder caution if markets misprice risk or conversely provide the liquidity needed to revitalize traded volumes. The central question is whether investors will embrace these new bonds at spreads commensurate with their risk or demand hefty discounts until uncertainties fade.

Why Treasuries Remain the Safer Harbor

U.S. Treasuries continue to offer a compelling alternative with steadily declining yields in the short-to-intermediate tenor, reflecting investor confidence in federal credit and predictable monetary policy maneuvers. Treasury yields falling by up to six basis points across various maturities demonstrates a market positioning favoring liquidity and the highest-grade assets.

In contrast, municipal yields have increased slightly, sending a muddled message about risk perception. The stubbornly elevated muni-Treasury yield ratios indicate that despite tax advantages, munis are not seen by all as a superior investment at this stage—largely due to concerns over credit quality, political entanglements, and the uncertain trajectory of interest rates.

Investor Implications: Patience and Selectivity Required

Given these complex forces, investors with a center-right approach to risk and a focus on fiscal prudence should evaluate munis with a more critical eye than usual. Rather than chasing headline yields or assuming muni safety by default, a rigorous analysis of issuer credit fundamentals, state and local fiscal health, and political risk factors is paramount.

Patience is a virtue, but only to a point. Capital allocation should remain conservative, favoring high-grade issues with clear revenue streams and manageable debt loads. The market’s current sluggishness demands selectivity—blind enthusiasm risks exposure to credit deterioration or valuation traps.

In all, while muni bonds may offer alluring yields in a low-growth world, they remain tethered by macroeconomic uncertainty, subdued investor confidence, and a cautious market infrastructure reluctant to elevate valuations absent clear support from inflows or meaningful news catalysts. The muni market’s path forward will be anything but straightforward.