The current landscape of municipal bonds presents a landscape riddled with contradictions that demand a skeptical eye. While some industry observers hail recent fiscal resilience, a deeper analysis reveals underlying vulnerabilities that could unravel in a matter of months. The narrative of strength driven by Treasury market support and robust issuance flows must be viewed through a prism of caution. Elevated issuance levels—over $366 billion year-to-date—are not just signs of vitality but potential catalysts for oversupply, which, coupled with declining reinvestment flows and inflation concerns, threaten to test the market’s durability.

Furthermore, the steady decline in reinvestment amounts—from a high of $40 billion in August to a projected $20 billion this September—is not purely a sign of cautious optimism but a red flag signaling a potential drop in liquidity that could precipitate volatility. The greater dependence on institutional inflows, retail demand, and alternative asset classes like separately managed accounts underscores an evolving, but fragile, structure. If macroeconomic conditions deteriorate, particularly with hesitant Federal Reserve rate adjustments, the muni market’s resilience will face intense scrutiny.

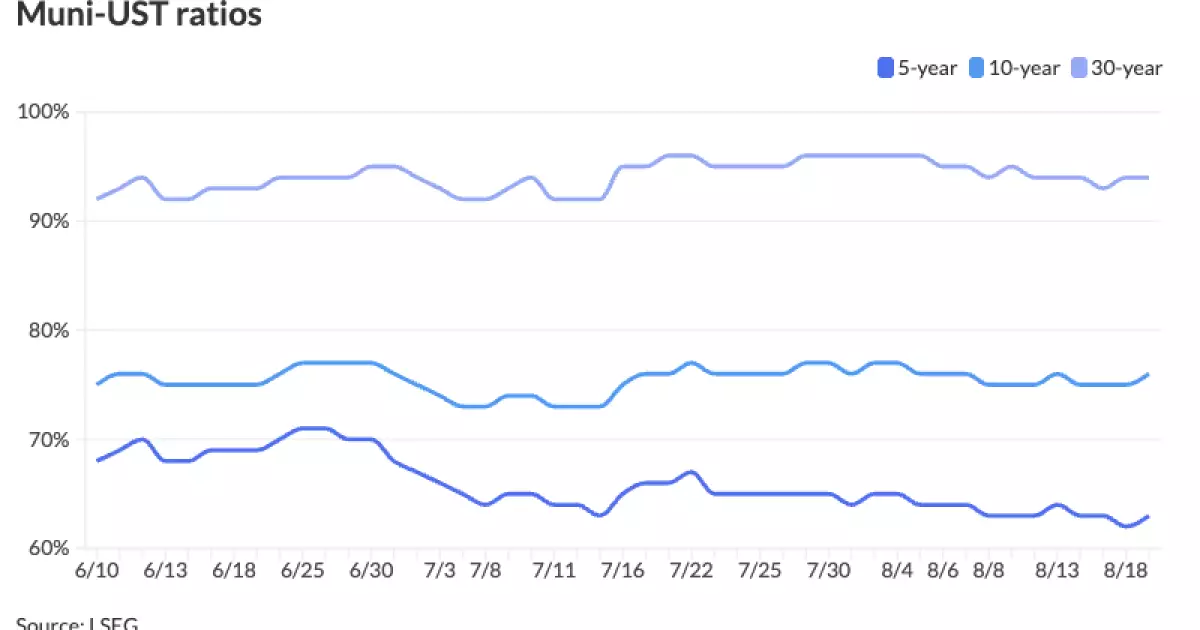

The rapid flattening and steepening of the yield curve, along with wider credit spreads, reflect a market in flux, grappling with external pressures such as inflation prints and geopolitics. Widening spreads are not merely a sign of risk premiums but could presage deteriorating credit quality among lower-rated issuers, especially as Hurricane season and other natural threats increase the chances of credit impairments in the coming months. These systemic risks are often masked in short-term data but loom larger when viewed from a longer-term perspective.

Deceptive Confidence in Primary Market Activity

Another critical concern lies in primary issuance. While issuers like Garland, Texas, and Maine State Housing Authority are tapping the market at seemingly attractive yields, it masks an underlying challenge: the market’s capacity to absorb Munis may be overstated. The bond prices reflect a market hopeful that demand will remain stable, but this assumption neglects the broader macroeconomic risks that threaten to dampen investor appetite soon.

The issuance pipeline—expected to reach between $575 billion and $600 billion this year—is staggeringly high, and historically, such elevated levels tend to lead to a correction. Even in an environment of seemingly robust demand from semi-institutional investors and retail platforms, this demand could fade if inflation pressures persist or if Washington politics introduce new regulatory or fiscal uncertainties. The assumption that demand from stable, income-focused investors will remain unwavering is naive; solely relying on investment behavior rooted in current yields ignores how shifting economic currents could catalyze withdrawals or restructuring.

Moreover, the market’s recent stability has been largely sustained by seasonal reinvestment strategies, not genuine growth in economic fundamentals. Once this reinvestment diminishes, the market’s true strength—or its vulnerability—will come into stark relief. The potential for defaults or credit downgrades in lower-rated sectors—such as high-yield municipal bonds linked to Brightline—remains an unspoken threat that could accelerate under adverse economic conditions.

External Pressures and the Future: A Tense Outlook

The external environment, notably the hurricane season and the broader inflationary backdrop, pose additional threats that are often underestimated. Natural disasters can devastate local economies, impair revenue streams, and increase default probabilities. As climate risks become more pronounced, the municipal sector’s lower-rated segments, which already operate within thin margin buffers, will be forced into uncharted territory.

Additionally, the upcoming Federal Open Market Committee (FOMC) minutes and their stance on future rate cuts could influence short-term demand for munis. The market’s current nervousness suggests that investors are poised to react swiftly if signals point to a more hawkish monetary policy trajectory. Rising yields, especially on the front end, could dampen retail and institutional enthusiasm just as the market’s liquidity is predicted to decline.

From a conservative perspective aligned with center-right liberalism, the fundamental issue is balancing fiscal prudence with the need for infrastructure investment. Over-reliance on debt issuance today risks creating a debt overhang that could hamper future growth. The municipal sector’s current strength is more indicative of strategic positioning rather than inherent resilience—market participants must remain vigilant, prepared for volatility that could emerge as macro conditions shift dramatically.

The municipal bond landscape is far from the safe haven it appears to be at first glance. Beneath the veneer of stability lies a tumult of risks—elevated issuance, waning reinvestment, external shocks, and political uncertainties—all poised to challenge even the most optimistic forecasts. For investors with a pragmatic, center-right liberal outlook, the message is clear: seize opportunities where they genuinely exist, but do so with caution, awareness, and a readiness to adapt to the inevitable volatility that lies ahead. In the world of munis, today’s perceived strength could swiftly morph into tomorrow’s crisis if prudent risk management is not prioritized.