In recent days, the municipal bond market has exhibited a mix of stability and shifting dynamics. On a particular Thursday, mutual funds in this space reported continued inflows while U.S. Treasury yields embarked on a slight upward trajectory. This article aims to explore the latest developments within this sector, scrutinize market trends, and provide insights into the implications for investors and municipal financing.

As of Thursday, municipal bonds were largely stable, characterized by minimal changes in yields despite an increase in U.S. Treasury rates. Specifically, two-year municipal to U.S. Treasury (UST) ratios remained consistent at around 62%, while longer maturities saw minor fluctuations, with the 30-year ratio standing at approximately 86%. These ratios suggest that while the outlook for UST may seem less favorable, municipalities continue to appeal to investors looking for steady returns amidst uncertainty.

The rise in UST yields, reportedly up to five basis points for longer-dated securities, has created a climate of cautious observation among municipal bond investors. According to market commentary, this shift in UST yields has not dramatically impacted municipal bonds, indicating a certain resilience. Portfolio managers like Kim Olsan have noted that a stronger demand for tax-exempt securities has been observed, particularly among maturities extending beyond 12 years. This segment of the market, showing a notable volume increase of 5% to 7% in recent trading, indicates a preference for longer-term investments, which can provide better yield pickups compared to shorter securities.

The ongoing trend of strong demand manifests itself through active trades in high-quality names, particularly state general obligations maturing in 20 years. These securities have become attractive due to their appealing pricing, allowing investors to secure assets with relatively favorable yield conditions. For instance, demand for Ohio general obligations due in 2043 demonstrated that investors are willing to pay a premium for long-dated bonds, seeking security in the face of market volatility.

Moreover, the upsizing of recent issuances in the primary market underscores a growing confidence. Notably, the South Carolina Public Service Authority’s bond issue was increased significantly from $650 million to over $1 billion in response to heightened investor interest. Similarly, the New York City Municipal Water Finance Authority adjusted its issuance size, marking a trend where strong demand leads to larger deals. Such patterns highlight the increasing appetite for municipal bonds, especially from in-state buyers who value the tax-exempt status of these investments.

Despite the current strength in the municipal market, analysts caution that the volatility observed may signal the need for a strategic approach as the upcoming March issuance/redemption cycle approaches. Negative supply projections could create interesting conditions for certain municipalities, particularly those like New York and New Jersey, which are anticipated to face challenges due to their respective net negative supply situations. This may result in rivalry among in-state buyers for the available bonds, further pushing up prices and tightening spreads.

California, recognized for its large negative supply projections, is also likely to experience tightening spreads as buyers vie for limited offerings. On the flip side, states such as Pennsylvania, showing a positive supply outlook, may witness widening spreads in their general obligations, indicating how differing supply conditions can affect investment strategies across states.

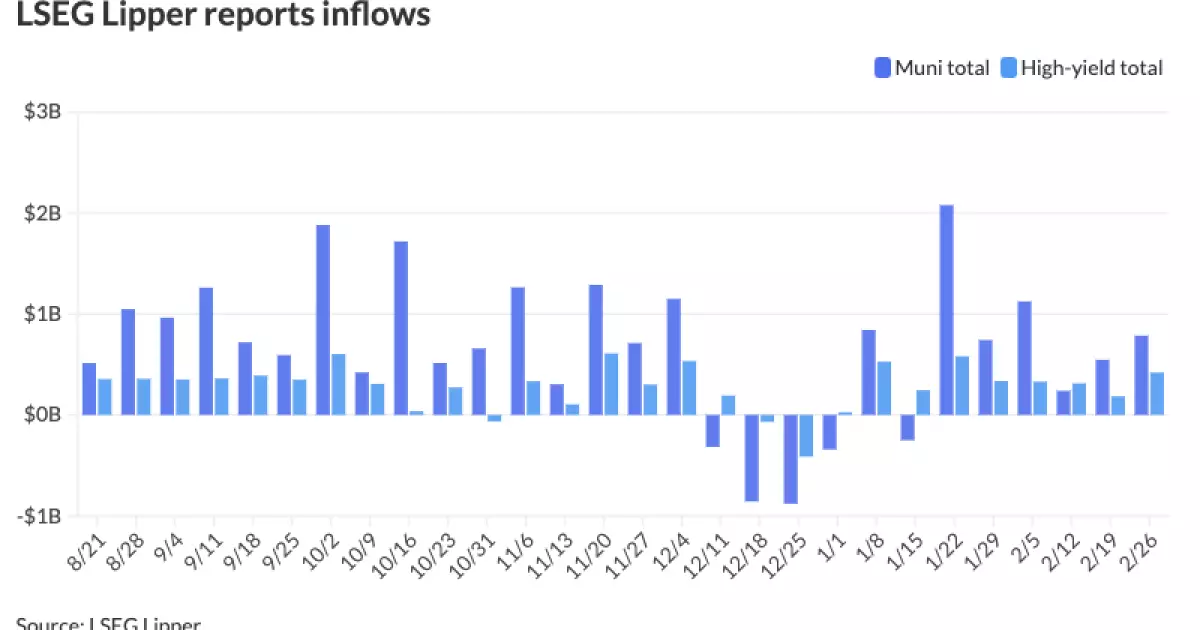

The bond market’s activity has not gone unnoticed by investors. Recent reports revealed that municipal bond mutual funds recorded inflows of approximately $785.5 million in a week, building upon previous gains. High-yield funds also enjoyed a solid influx, pointing to a broader trend of investor confidence in the municipal sector. In stark contrast, taxable money market assets saw significant withdrawals, indicating a shift in investor focus towards tax-exempt options that promise long-term stability.

In the competitive landscape, issuers such as the Massachusetts Development Finance Agency have taken steps to capitalize on market demand by pricing bonds that reflect current yield environments, ensuring that there is adequate supply to meet the investment appetite. As various municipalities navigate these complex market dynamics, it is evident that strategic planning remains key to success.

In the ever-evolving world of municipal bonds, the current trends underscore the complexity and resilience of this market. With investors showing robust demand for longer maturities, coupled with the upsizing of key deals, the landscape appears promising. However, as we venture into the next phase of market cycles, investors must remain vigilant, adapting their strategies to the changing tides of supply and demand. The dynamics within the municipal bond market present both challenges and opportunities, emphasizing the need for informed decision-making in pursuit of securing valuable municipal assets.