The recent inertia in municipal bond markets, characterized by minimal price fluctuations amidst seemingly stable yields, masks an undercurrent of systemic vulnerability. For decades, munis have been regarded as a safe haven for conservative investors, largely insulated from the turbulence faced by corporate or equity markets. However, a critical analysis of current market dynamics reveals that this serenity is, at best, superficial. The underlying issues—massive issuances, a decaying infrastructure, and shifting investor preferences—conspire to threaten the very foundation of municipal finance stability.

Despite appearances of calm, munis are exhibiting strange phenomena, including steepening yield curves and underperformance relative to other fixed-income assets. Notably, the long-term muni sector, especially bonds with durations beyond 22 years, has experienced a notable decline—nearly 4% year-to-date—an anomaly in the context of rising or stable markets. Such persistent underperformance, juxtaposed with gains elsewhere, signals deeper structural problems that warrant skepticism rather than complacency.

Supply Surges and the Myth of Tax Exemption Preservation

One striking feature exacerbating munis’ woes is the enormous surge in issuance volume. With approximately $280 billion in bonds flooding the market during the first half of the year, the supply glut has depressed prices, particularly on the long end. The initial panic—driven by fears over potential elimination of tax exemptions—prompted issuers to schedule and expedite offerings, effectively frontloading supply. Ironically, the anticipated threat—the ‘One Big Beautiful Bill’—was successfully neutralized, leaving this massive issuance wave as an overhang on the market.

This narrative illustrates how market psychology and political uncertainty have temporarily distorted the muni landscape, but it also highlights how the actual threat to tax-exempt status was overstated. Now, with the tax exemption intact, the question arises: are those massive issuances going to unwind, and will the market absorb this backlog without further damage? The answer remains uncertain. Although the bill’s passage should temper issuance, the aftermath of such a boom is often a prolonged adjustment period during which prices remain fragile.

What’s Driving the Anomaly? Supply, Fund Flows, or Structural Change?

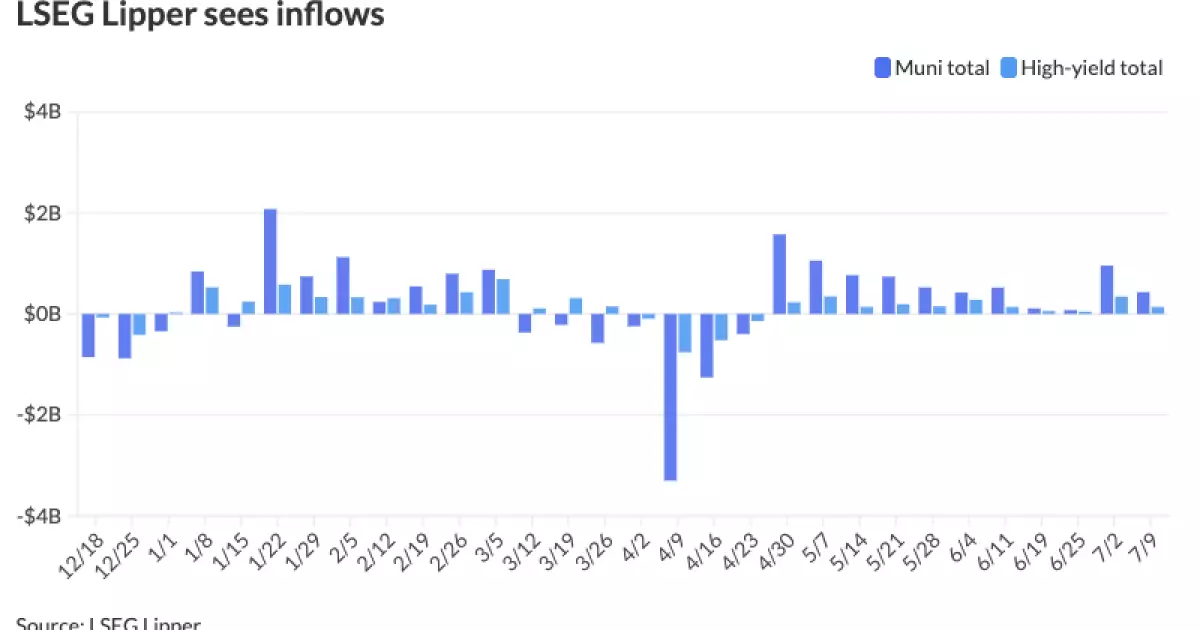

Several factors contribute to the current disconnect between muni performance and other asset classes. Foremost is supply; the surge in issuance, coupled with sluggish demand, especially on the long end, has distorted the yield curve, making muni bonds appear less attractive. Importantly, the data indicates that fund flows are predominantly into shorter maturities—typically less than 15 years—with investors avoiding extensions into the 20- or 30-year range. This preference reflects a growing wariness of long-term vulnerabilities, perhaps foreshadowing a structural shift.

Fund flows, however, are not solely driven by investor preferences but also by strategic repositioning in anticipation of monetary policy shifts. With the Federal Reserve potentially cutting rates in the near future, there’s a growing probability that short-term yields will decline, prompting a rally into munis. Nevertheless, the long end remains under pressure, perhaps indicating a market consensus that long-term risk factors—potential inflation, infrastructure deterioration, and political instability—are more significant than the current yields suggest.

The question is whether these anomalies are temporary distortions or indicators of a fundamental shift in how municipal debt markets operate. The steepening curve and underperformance of long munis could be warning signs of coming turbulence, or simply a phase of market recalibration. Given the political and economic climate, particularly in regions heavily reliant on infrastructure spending, the risk of a deeper systemic crisis should not be dismissed.

The Political and Economic Implications of Market Divergence

From a political standpoint, the muni market’s health is often viewed through the lens of local government stability, fiscal discipline, and infrastructure adequacy. A widening of the yield curve and the decline of long-term bonds signal that investors are increasingly skeptical of the long-term fiscal sustainability of certain issuers. This skepticism mirrors broader concerns about aging infrastructure, rising debt burdens, and the erosion of dedicated tax revenues.

Economically, the market’s current condition contradicts the bipartisan narrative of fiscal prudence. Despite assurances that the tax exemption remains secure, the market’s underperformance indicates that investors are pricing in potential future risks—be it inflationary pressures or federal policy changes. It suggests that the traditional ‘risk-free’ status of munis is no longer guaranteed and that policymakers need to rethink the infrastructure financing model.

Moreover, the reliance on short-term fund flows and tactical positioning points to a fragile confidence foundation. The shift away from long maturity bonds could accelerate if investors begin to reassess the true risk profile of local governments and their ability to meet debt obligations under changing fiscal regimes. This could foster a vicious cycle of rising yields and worsened market sentiment, especially if the economy experiences a downturn.

While the market currently presents an illusion of stability, a critical examination underscores the importance of vigilance. Thousands of local governments, driven by short-term needs and political pressures, have borrowed heavily, often without sufficient oversight or sustainable revenue streams. The recent market behavior, characterized by steepening curves and underperformance, signals an erosion of confidence that could have far-reaching implications.

Investors and policymakers alike must recognize that the municipal bond market is at a crossroads. Without meaningful reforms—improved transparency, fiscal discipline, and strategic infrastructure investment—the sector risks unraveling when economic or political shocks occur. The current complacency, masked by a calm facade, belies a deeper crisis waiting to surface if true fiscal health is not addressed.