Despite the superficial appearance of stability in the bond markets, a deeper examination reveals a fragile structure susceptible to abrupt shifts. The recent lull—characterized by muted movements in munis and Treasuries—can be dangerously deceptive. On the surface, yields are inching upward, signaling minor corrections after prolonged rallies. However, these ostensibly “small” rises may be masking a more profound underlying risk: a market that has become overextended, lulled into complacency by recent gains.

The so-called “quiet” phase is often a precursor to instability. Market participants, lulled into believing that yields are levelling off, tend to ignore the signs of overbuying and excessive optimism. While strategists like Tim McGregor acknowledge a potential pullback, this retreat might not be sufficient to address the underlying vulnerabilities. In fact, the complacency embedded within the current market sentiment could amplify the severity of the inevitable correction—particularly if macroeconomic conditions deteriorate unexpectedly.

Speculative Behavior and Investor Overconfidence Inflating Valuations

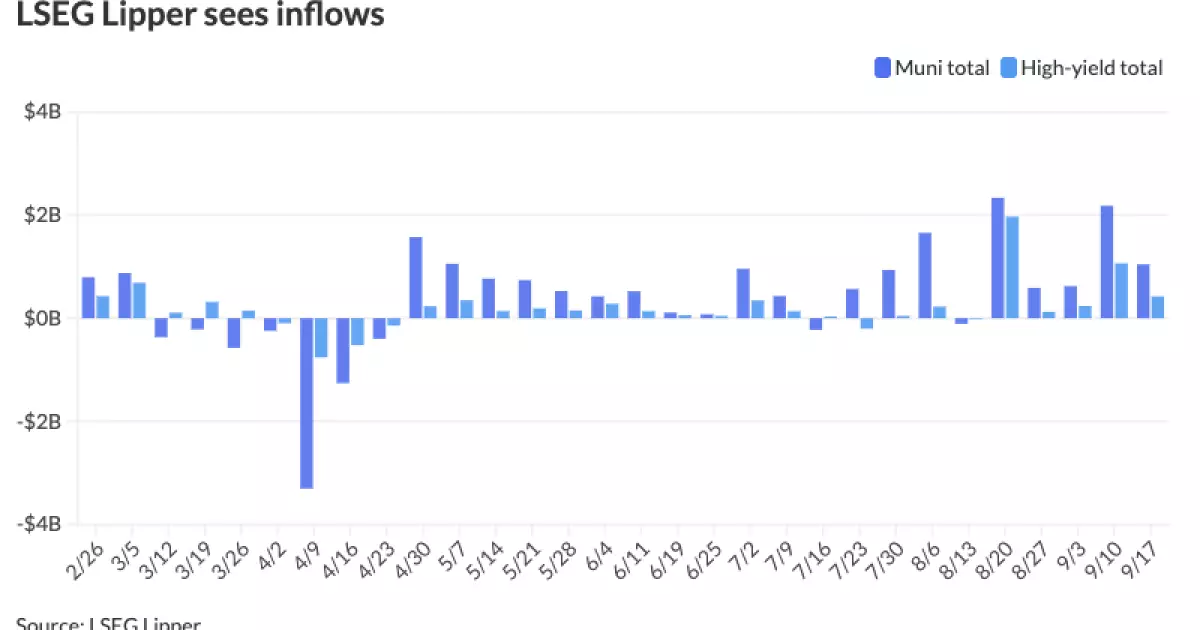

The fervor surrounding munis and taxable bonds is largely driven by narrative-driven optimism rather than fundamental stability. Investors are increasingly attracted to the allure of positive returns, leading to a surge in mutual fund and ETF inflows. Such inflows—totaling over $1 billion in recent weeks—paint a picture of robust confidence. Yet, this faith is misplaced if it disregards the potential risks embedded in these high valuations.

The rally in muni bonds, especially long-term issues, has been characterized by aggressive extension strategies that reward prolonged-term holdings. But this outperformance is not sustainable. The evident steepness of the muni curve—more than double that of UST—indicates a market overly reliant on perceived safety, even as yields creep toward historically low levels. When yields for AAA-rated bonds dwell near or below 2%, it raises the question: are investors truly getting value or merely chasing yield in a market plagued by distortions? This chase inflates prices, creating a bubble that is vulnerable to a sharp correction.

Furthermore, risk-taking has been notably encouraged within lower-credit ratings—particularly Baa-rated bonds—where gains are outpacing those of higher-rated securities. This tilt towards riskier assets, under the guise of value, enhances systemic vulnerabilities. When macro shocks materialize, the market’s overconfidence could turn into panic, causing a rapid devaluation of these overleveraged positions.

Government Policies and Economic Slowdown: The Hidden Traps

Adding to the precariousness are macroeconomic realities that seem to conflict with the facade of a thriving bond market. The potential for a new easing cycle, hinted at by some market analysts, could encourage further risk-taking—yet, in reality, it might merely postpone inevitable corrections.

Government policies—particularly fiscal stimulus or monetary easing—often have a reputational effect rather than a tangible fix. If policymakers adopt a staggered or cautious approach, it could lead to increased supply of long-duration bonds, pressuring prices downward. The upcoming surge in supply, combined with a possible economic slowdown, could catalyze a swift decline in bond valuations.

Furthermore, inflationary pressures and rising interest rates—evidenced by Treasuries climbing steadily—are fundamental risks that threaten to burst the complacency bubble. The market’s current low-yield environment is artificially sustained, but the risk of a sudden spike in inflation could render these valuations unsustainable. When that occurs, markets may face a sharp reappraisal, leading to significant losses for those who bought into the current optimistic narrative.

The Fallacy of Liquidity and the Illusion of Safety

Another critical flaw in the current market structure is the overreliance on liquidity and the perceived safety of municipal bonds. The recent increase in CUSIP requests and the sizable share of short-term trades suggest a market awash with activity—yet this activity is not necessarily indicative of health. Instead, it highlights a scramble for yield in a low-return environment, often at the expense of solid fundamentals.

The liquidity appears robust, but this is a double-edged sword. The steadiness of the SIFMA Swap Index, which has remained within a narrow range, masks the underlying risk of a sudden liquidity crunch. If market sentiment shifts or macroeconomic shocks arrive, the unwinding of positions could happen swiftly, leaving investors holding assets that are far less liquid than they appear.

Moreover, the widespread belief that munis are safe is increasingly challenged by structural vulnerabilities—states and municipalities facing budget constraints or credit downgrades—yet these risks are often downplayed by market commentary. The assertion that munis are “good returns” without recognizing fiscal fragilities presents an overly optimistic narrative that could encourage blind risk-taking.

The Imminent Challenge of Rising Supply and Demand Imbalance

The upcoming influx of supply—expected to spike in the fall—poses a significant threat to market stability. The considerable increase in issuance, especially from states like Texas and New York, will test investors’ appetite for bonds at these historically low yields. When supply outpaces demand, prices naturally decline, shifting the risk of loss to those whose models are based on continued appreciation.

This dynamic is compounded by the persistent chase of yields—investors are willing to accept ever-lower returns for perceived security. This relentless pursuit inflates bond prices to unsustainable levels, setting the stage for sharp corrections. The “rich valuations” across short and medium-term securities suggest that there is little buffer left for error; a misjudgment or macroevent could trigger rapid sell-offs.

In assessing the broader picture, the bond market’s current trajectory aligns with a classic pattern of overconfidence leading to eventual correction. The extended rally, driven by a mix of technical factors and behavioral biases, has created an environment vulnerable to volatility. A cautious stance—recognizing the perilous overextension and the inherent risks of complacency—is vital to avoiding substantial losses when the inevitable correction arrives.